Tax News - June 2023

Applicable changes in tax legislation

I. INCOME TAX ACT

Taxation of cross-border migrant workers is not incompatible with the Constitution

A group of members of the parliament from the NSI and SDS has filed a petition to review the constitutionality of Articles 44 and 45 of the Income Tax Act (ZDoh-2). The petitioners consider that the contested regulation in the assessment of income tax on income from employment results in unequal treatment of Slovenian tax residents, working in Slovenia for a Slovenian employer and Slovenian tax residents, working abroad for a foreign employer in the. The latter should receive a lower disposable income after tax deduction due to the different tax treatment of reimbursement of travel and meal expenses.

The Constitutional Court did not find any incompatibility with the Constitution in these claims. In the opinion of the Constitutional Court judges, the effect of the contested provisions of the law on the tax base for the calculation of income tax on the income from employment is the same for cross-border migrant workers and other taxpayers. Therefore, the contested provisions are not incompatible with the Constitution, they added.

II. PAYROLL

Flat-rate contributions for special cases in 2023

The Decision on the determination of contributions for special cases of insurance, which sets the amounts of the flat-rate contributions from 1 April 2023 onwards, is published in the Official Gazette of the Republic of Slovenia No 30/2023.

Type of flat-rate contribution | Amount from 1.4.2022 to 31.3.2023 | Amount from 1.4.2023 onwards |

For insured persons referred to in second, third, fourth, fifth and sixth indents of the third paragraph of Article 20 of Pension and Disability Insurance Act (PDIA-2) (persons performing practical work, voluntary practice after school, vocational rehabilitation, training, etc.) | EUR 8.23 per month | EUR 8.46 per month |

For insured persons referred to in the first and tenth indent of the third paragraph of Article 20 of PDIA-2 (pupils, students on compulsory and voluntary work placement) | EUR 12.31 per month | EUR 12.65 per month |

For insured persons referred to in paragraph 4 of Article 20 of the PDIA-2 (persons serving sentences, minors subject to educational measures) | EUR 16.39 per month | EUR 16.85 per month |

For the insured persons referred to in the first indent of the first paragraph of Article 20 of PDIA -2 (persons independently performing activity and not insured under Article 15 of PDIA -2) and for the insured persons referred to in the second paragraph of Article 20 of PDIA -2 (persons carrying out an agricultural or forestry activity who are not insured under Article 17 or Article 25 of PDIA -2) | EUR 41.04 per month | EUR 42.19 per month |

For insured persons referred to in the eighth indent of the third paragraph of Article 20 of PDIA -2 (accommodation providers who occasionally, or for a maximum of 5 months, carry out such activity, and are not insured under Article 15 of PDIA -2) | EUR 205.20 per year or EUR 17.09 per month | EUR 210.95 per year or EUR 17.57 per month |

for insured persons referred to in Article 20(5) of the Social Insurance Act (persons in the course of organized activities) | 4,07 EUR per year | 4,18 EUR per year |

Holiday allowance

A holiday allowance is a benefit that an employer must pay to an employee in addition to annual leave. The minimum amount of the annual leave allowance is set by the Employment Relationships Act (ERA-1), which stipulates that the employer is obliged to pay the holiday allowance for annual leave to an employee who is entitled to annual leave. It must be paid by 1 July, however, in the event of the employer's illiquidity, a collective agreement at industry level may set a later deadline for the payment of the annual leave allowance, but no later than 1 November.

The ERA-1 also stipulates that the amount of holiday allowance must be paid out at least in the amount of a minimum wage. As the minimum wage for 2023 is EUR 1,203.36, this is also the minimum amount of the holiday allowance payment for 2023. This payment is tax-free up to the amount of the average wage in the Republic of Slovenia in the month in which it is paid, which means that it is exempt from contributions and income tax. The amount of the average wage taken into account changes every month, the data according to the average wage each month is published by SURS.

In the private sector, however, the amount of the 2023 holiday allowance depends on the employer. The ERA-1 only sets a minimum amount for 2023. However, collective agreements must also be considered. If the amount of the 2023 holiday allowance in collective agreement is higher in comparison with ERA-1, the holiday allowance is paid as set out in collective agreement.

If the worker is not employed for a full calendar year, he is not entitled to the full holiday allowance, but only to a proportion, which depends on the number of months for which the employment contract is concluded and consequently to the right to take a pro-rata share of annual leave.

Compensation for using your own tools at work

Compensation for the use of workers` own tools, appliances, and objects (other than personal vehicles), necessary for the performance of work at the workplace, is not included in the tax base of income from employment, provided that:

- are determined by specific regulation and collective agreement or an employer's internal act,

- used tools are inherent, necessary and customary for the performance of particular work,

- the compensation is based on a calculation of true costs and represents a fair and reasonable amount,

- the amount does not exceed 2% of the employee's monthly salary or 2% of the average monthly salary of employees in Slovenia.

If the employer pays compensation in an amount, higher than non-taxed amount under Article 44(6)(1) of the Personal Income Tax Act (PITA-2), the amount of (excess) income above the non-taxed amount is included in the taxable amount of the income from employment.

Compensation for the use of own resources when working from home

A worker's right to the compensation for the use of own resources during work from home is established by Article 70 of the Employment Relationships Act (ERA-1), which provides in its second paragraph that the amount of the compensation is determined by the employment contract.

The amendment to Personal Income Tax Act (PITA-2AA) (Official Gazette No 158/22) amends, effective from 1 January 2023, the provision of Article 4(1)(10), according to which compensation for the use of own resources in home-based work (in accordance with the regulations governing employment relationships, provided that it is determined by special regulations or on the basis of a collective agreement or general act of the employer) shall not be included in the tax base from income from employment relationship up to the amount of 0.20% of the last known average annual salary of employees in Slovenia, calculated on a monthly basis, for each day of work from home. Taking into account the last known average salary, published by the Statistical Office of the Republic of Slovenia for the year 2022 (2.023,92 EUR), the amount that shall not be included in the tax base is EUR 4,05 per day as from 24 February 2023 (until 23.2.2023, the amount of the allowance was EUR 3,94 per day).

The amount of compensation, exceeding the statutory amount, is included in the employee`s tax base from income from employment.

National Assembly approves detailed recording of working time record

On 21 April 2023, the National Assembly approved (by 52 votes to 16) the amendment to the Labour and Social Security Registers Act (LSSRA), which anticipates recording additional information on working time records and introduces mandatory electronic records for offenders with no exception.

The Ministry of Labour stressed, at the time of the adoption of the amendment, that the changes had been called for by the Labour Inspectorate for many years, due to numerous working time-related violations, and that the solutions had been coordinated with the social partners.

They underlined keeping daily records of working time has already been compulsory in the form of the number of hours worked, but that more detailed information would now have to be recorded, such as the time of arrival and departure from work, the use of breaks, the hours worked in special conditions and in irregularly distributed working hours, etc. They will have to be kept either in writing or electronically, however, electronic recording will only be compulsory for those who violate labour law.

The new measures also include employer`s obligation to inform (in writing) the employee of the information, kept in the working time record, for the previous month, and the right of the employee to request from employer to inform him (in writing) of the information, kept in the working time record, once a week.

There is also a new definition of a employee – employee is anyone who performs work for an employer on a legal basis, provided that the work is performed in person and that the worker is involved in the employer's work process or mostly uses employer`s tools and resources during work process.

Adoption of new Act on transnational provision of services

On 22 March 2023, the National Assembly adopted a new Transnational Provision of Services Act (TPS-1), which entered into force on 18 April 2023.

The new Act transposes EU Directive 2020/1057 and newly implements three Regulations: Regulation (EC) No 1072/2009, Regulation (EC) No 1073/2009 and Commission Regulation (EU) 2016/403 supplementing Regulation (EC) No 1071/2009.

The new Act applies to all legal entities and natural persons (registered to perform business activity) established in Slovenia and providing services in another EU country and vice versa. These persons may temporarily or occasionally provide services in another country but must obtain an A1 certificate for their workers before providing services.

According to Article 4 of the Act, an employer may provide cross-border services, if he meets the following conditions:

- performs business activity in the Republic of Slovenia,

- does not violate provisions of labour law relating to the workers` rights,

- services are provided in the context of an activity for which the employer is registered in Slovenia, except in case of posting workers to a related company, and

- services are provided on own account and under own management on the basis of a contract with the client, act of posting workers to a related company or in the context of the activity of providing workers to the user.

The same conditions apply to the self-employed.

Under the Act, employers or the self-employed are obliged to apply for an A1 certificate prior to the commencement of services or at the latest on the day of providing services. A new feature is that both are now obliged to inform the Health Insurance Institute of the Republic of Slovenia (ZZZS) of any changes on an ongoing basis, within 5 days of such changes occurring.

The application for the A1 certificate is submitted via SPOT portal, which is also used for submission of other notifications, determined by the Act.

According to the new provisions, the exercised right of a worker to rest, vacation leave or a short period of absence due to sickness shall not be considered as interruption of the transnational provision of services or an interruption of workers` posting.

Third-country citizens (posted workers or the self-employed) may now provide services in the EU on the basis of a valid uniform (single) residence and work permit or a temporary residence permit which is not issued for the purpose of employment, self-employment or work, provided that the foreigner has the relevant consent of the Employment Service of the Republic of Slovenia or, on the basis of the Employment, Self-employment and Work of Foreigners Act, they have the right to freely access the labour market.

The Act does not introduce any new conditions for the issuance of A1 certificate for the purpose of transnational provision of services in one EU Member State, but in line with European legislation, it introduces new conditions for the issuance of an A1 certificate for the purpose of cross-border provision of services in at least two EU Member States, which apply to both, employers and the self-employed. In addition to conditions on national level, applicants for an A1 certificate must also submit a statement under criminal and material liability that the person for whom the A1 certificate is issued is expected to carry out the work or self-employed activity in at least two EU Member States.

The applicant (or the person for whom the A1 certificate is obtained) may, on the basis of A1 certificate, carry out work or self-employment activity for a maximum of the following 12 calendar months, however, the new Act also provides possibility of extending the period to 18 months.

The Act also regulates the transnational provision of services by foreign employers and foreign self-employed persons in the Republic of Slovenia. In this part, the legislator has also anticipated some changes regarding obligations of the foreign employer and the posted worker or driver in the transnational provision of services, namely that before the foreign employer starts providing the service, he/she must register at the Employment Service of the Republic of Slovenia. In addition to already required information, address (or, in case address is not available, GPS-coordinates of the location where the service will be provided) is now also required.

III. VALUE ADDED TAX

Amendments to the Fiscal Validation of Receipts Act (FVRA)

On 18 April 2023, the Act on Amendments and Additions to the Fiscal Validation of Receipts Act (Official Journal of the Republic of Slovenia, No 40) enters into force, reintroducing the obligation to hand over an invoice to the buyer - the final consumer - for the goods purchased or services received.

From 18 April 2023 on, the taxable person must always hand over the invoice to the customer (not only at the customer's request), irrespective of the method of payment.

The invoice may be delivered to the customer in paper or electronic form. The most common electronic form, possible due to modern technology, is the transmission of the invoice to the customer by means of a mobile application or by e-mail. If the buyer paid in cash, then the invoice must be given in both, paper and electronic form, before the buyer leaves the seller's premises, in which the acquired goods or provided services were paid for.

The buyer must take the invoice and, if the payment was made in cash, retain it when leaving the taxable person's business premises.

In case when electronic invoice is issued, the customer must take the invoice and retain it after leaving the business premises (in case of a cash payment) and submit it to an authorized person of the tax or marketing authority on request.

No increase in VAT rates announced by the government

In a press release published on its website on 25 April 2023, the Government of the Republic of Slovenia, in order to avoid other interpretations, clarifies that the Stability Programme 2023 document does not foresee an increase in the value added tax (VAT) rates.

Expiry of the period of reduced VAT rate for energy sources

At the end of May, the period, during which the VAT rate on the supply of electricity, natural gas, firewood and wood for district heating for all users was reduced from 22% to 9.5%, has expired. At this stage, it is not known whether it will be extended or not. However, a possible extension of the reduced VAT rate would require a further amendment of the law, but a draft of such a legislative proposal is currently not included in any of the government's materials.

Even if the government decides to propose a new law, it would only be approved in the National Assembly during June at best and would have to apply retroactively for a continuous period of reduced VAT. This is not common practice in tax matters due to the challenges it brings in accounting.

However, if the government does not opt for an extension, bills for these energy products will be higher from July onwards, regardless of the fact that the government has extended the regulation of retail electricity and gas prices for households, small business and sheltered customers, and electricity prices for small and medium-sized enterprises until the end of the year.

IV. EXCISE DUTIES

Increase in excise duties on tobacco products and obligation to account for the difference between excise duties on fine-cut tobacco and cigarettes

Decree determining the amount of excise duties on tobacco products (Official Journal of the RS, No. 151/2022), which was issued on 2 December 2022, determines an increase in the amount of excise duty on tobacco products under Article 86 of the Excise Duty Act (Official Journal of the RS, No. 47/16, as amended) as of 1 May 2023.

In accordance with the above-mentioned legislation, the excise duty on tobacco products shall be as from 1 May 2023:

- proportional excise duty of 23.91 % of the retail selling price of a packet of cigarettes,

- a specific excise duty of EUR 86.62 per 1000 cigarettes. However, if the retail selling price of a packet of 20 cigarettes is lower than EUR 4.12, an excise duty of EUR 136 per 1000 cigarettes shall be paid;

- for fine-cut tobacco: 38% of the retail selling price and EUR 54 per kilogram, but not less than EUR 114 per kilogram;

- for cigars and cigarillos: 6.4% of the retail selling price, but not less than EUR 54 per 1000 pieces;

- for other smoking tobacco: EUR 54 per kilogram;

- for heating tobacco: EUR 116 per kilogram of filter tobacco; and

- for electronic cigarettes: EUR 0.21 per milliliter of nicotine liquid and EUR 0.10 per milliliter of non-nicotine liquid.

Change in excise duties on energy products and electricity

At a correspondence meeting on 24 April 2023, the Government adopted an amendment to the Decree determining the amount of excise duty on energy products and electricity, which amends the excise duty on unleaded petrol, gas oil for power (diesel) and gas oil for heating (extra-light heating oil - KOEL).

The government has adjusted the excise duty on these energy products so that the final retail prices of unleaded petrol and gas oil for power (diesel) will remain unchanged, while the retail price of gas oil for will slightly decrease.

The excise duty on unleaded petrol is thus changed from EUR 0.388 per liter to EUR 0.412 per liter, from EUR 0.423 per liter to EUR 0.443 per liter on gas oil for power (diesel) and from EUR 0.127 per liter to EUR 0.133 per liter on gas oil for heating (KOEL).

The Government is closely monitoring the situation on the oil derivatives` market and is adjusting the level of excise duties in order to maintain the retail prices affordable, while at the same time aiming at a gradual normalization of the inflows to the State budget in aspect of public financial sustainability. In the latter case, it is important to reintroduce environmental taxes on fossil fuels, which are a dedicated source of green investments, in the medium term and gradually, without consumers feeling the impact.

V. ACT AMENDING FOREIGNERS ACT (AAFA-2)

On 28 March 2023, the National Assembly adopted the Act Amending the Foreigners Act (AAFA-2), which entered into force on 27 April 2023, the day after its publication in the Official Gazette of the Republic of Slovenia.

The Foreigners Act (FA-2) establishes the conditions and manner of entry, departure and stay of foreigners in the Republic of Slovenia, while the essential solutions introduced by AAFA-2 are as follows:

- for the provision regarding the renewal of temporary residence permit for family members of foreigners and condition for issuance of permanent residence permit (passed Slovene language exam), the date of entry into force has been postponed to 1 November 2024, whereas previous period applies,

- the reintroduction of free funding for Slovenian language courses for all categories of foreigners who were eligible for free funding before the adoption of FA-2F,

- to relieve administrative units, the possibility of personal delivery by post is added for temporary residence permits (during the course extension and re-issuance) and for permanent residence permits,

- the storage of biometric data on foreigners' facial image and fingerprints is also envisaged for the purpose of unique identification of the foreigner in the procedure of renewal and further issuance of temporary residence permit and for renewal of certificate of the rights of a border-zone worker,

- the concept of deciding whether to change workplace at the same employer, to change employers or to be employed by two or more employers is being changed. Namely, written approval in the form of a decision is abolished and replaced by the consent of the Employment Service of the Republic of Slovenia,

- the “one-stop-shop” principle is introduced in the procedure for issuance of residence and work permits, according to which the foreigner or his/her employer submits a single residence and work permit application to the administrative unit or to the competent diplomatic mission or consulate of the Republic of Slovenia abroad,

- the possibility of crossing the state border in cases, where a foreigner has submitted an application for the extension or further issue of a residence permit and the application has not yet been decided but the foreigner has left the Slovene territory, is added, thus allowing foreigners, who do not require a visa to enter the Republic of Slovenia, to be able to enter the Republic of Slovenia during the period of the decision on the application, in accordance with the purpose for which they will receive a temporary residence permit,

- abolition of the compulsory six-monthly periodic verification of the fulfilment of the condition of sufficient resources for subsistence ex officio by the administrative unit.

The AAFA-2 emphasizes the principle of procedural economy and pursues the objective of eliminating unnecessary administrative obstacles, thus providing the basis for faster resolution of administrative matters covered by the FA-2 that fall within the competence of administrative units, which will contribute significantly to reducing the backlog in this area.

VI. OTHER CHARGES

Slovene Tax Authority (STA): Be cautious when opening a business in Bosnia and Herzegovina (BIH) - risk of involvement in tax evasion!

On 13 March 2023, STA published a notice due to the increasing number of ads by tax consultants offering to open a business in BIH. While tax consultants often claim that this is merely tax optimization, STA notes that this is not the case and that, as a consequence, individuals and companies may be involved in tax evasion. Tax consultants usually offer a comprehensive service, with the preparation of act of establishment, document authentication, registration at the court, opening a business account at a bank, obtaining tax number, renting of business premises and the establishment of a company headquarters, temporary residence registration, work permit acquisition and other business activities.

Tax consultants thus portrayed the opening of a business in BIH as a tax optimization, i.e. a legally permitted practice that allows for tax savings. Tax savings are mainly a consequence of the difference in statutory taxation in BIH, which is supposed to be more favorable than in Slovenia, due to lower tax on profit (10%) and VAT (17%), while dividends, vehicles and vessels are not taxed.

STA stipulates that the establishment of a company by Slovene citizens outside Slovenia is not always controversial. However, this is only the case where such companies have real economic substance for performance of activity. It is essential that the company literally carries out the activity and the services are provided.

If this is not the case, we are talking about aggressive tax planning, which can also lead to tax evasion. Slovene companies should be aware that they can achieve positive tax effects only if they fundamentally change the way they do business.

STA also noted that it will pay particular attention to companies established in BIH and possible abuses related to them, both, in terms of correct taxation of the business entities and correct taxation of the individuals behind the scheme who actually profited from the disputed transactions.

Constitutional Court suspends implementation of the controversial part of the Act Amending the Financial Administration Act (AAFAA)

In the context of a request for a constitutional review, filed by the Human Rights Ombudsman, the Constitutional Court temporarily suspended the implementation of a controversial provision of the AAFAA, according to which the STA may use technical devices in financial investigations to obtain data on recording and movement of goods without a court decision.

The Constitutional Court weighed the possibility of the occurrence of irreparable consequences in the case of the use of technical devices, if the provision was subsequently found unconstitutional in a constitutional judicial review, against the possibility of the occurrence of irreparable harmful consequences, if the implementation of the contested regulation was suspended and the law was subsequently found to be compliant with the Constitution.

According to the Constitutional Court judges, neither the Government nor the National Assembly has been able to demonstrate that the conduct of financial investigations would be completely prevented, while, on the other hand, the exercise of the powers, contained in the amendment, could lead to harmful consequences for individuals, which go to the fundamental of how national authorities function.

The Constitutional Court judges unanimously adopted decision on a temporary suspension while at the same time decided that the Court would give absolute priority to the request for a review of the constitutionality of the aforementioned article.

New valorization coefficients for the recalculation of the bases from previous years of insurance to the level of the average salary per employed person paid for year 2022

The Ministry of Labour, Family, Social Affairs and Equal Opportunities, in agreement with the Ministry of Finance, published the valorization coefficients for the conversion of the bases from previous years of insurance to the level of the average salary per employed person paid for 2022. Namely, bases from previous years of insurance, when determining the pension base for the assessment of pensions effective in 2023, are recalculated in advance to correspond to the level of the average salary paid in 2022, by recalculating the average monthly base from the year with the corresponding valorization coefficient for that year. The table of valorization coefficients is available in the Official Gazette of the Republic of Slovenia No 37/2023 of 29 March 2023.

New SIAES2 implementation notice

On 24 May 2023, the STA introduced SIAES2, a new system for filing export declarations. As a result, filing export declarations via the e-export application is no longer possible as of 24 May 2023. Users of the application are urged to ensure that they have the possibility to file export declarations via software providers on the market.

Submission Overview (Traffic light) - new eService

The Submission Overview is a new eService that allows the eTax user to view information on the submitted or not submitted for all represented entities. The user can only see in the overview the information on submitted or not submitted documents, for which the EDP has the right to file the document. Currently, the submission overview includes the DOD-DDPO form and the DDD-DDD form. Other forms will be added by STA gradually.

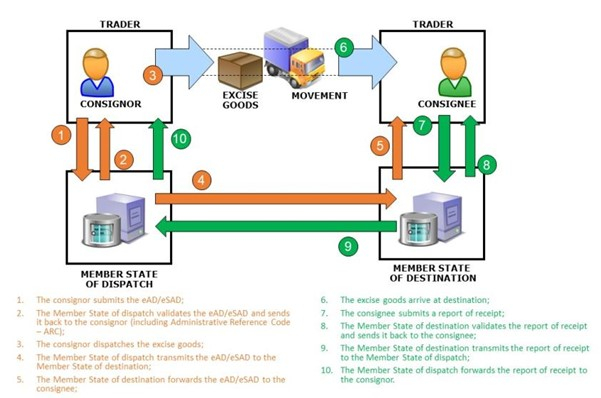

Excise Movement and Control System (EMCS)

From 13 February 2023, the use of the electronic Simplified Administrative Document (e-SAD) for the movement of excise goods for commercial purposes and fully denatured alcohol between Slovenia and EU Member States is mandatory.

Economic operators are electronically linked to the EMCS; depending on their business and excise status, they may:

- (consignors) enter and submit the e-AD and, if necessary, correct it and receive a report of receipt;

- (consignees) receive the e-AD and enter and submit a report of receipt.

Each entity shall use the interface to the system provided by its national administration. In our case, this is the e-Customs portal.

In some cases where energy products are not subject to excise duty (no excise duty is paid), their movements must still be reported via EMCS.

The picture below shows the process.

*****

Want to stay updated via email?

Subscribe to our free Tax News newsletter.

Want to know more?